Why Life Insurers should be making fact-based decisions

As technology becomes more of a feature in the average consumer’s everyday life, they increasingly expect their financial service providers to adapt to their needs. This transition to a digital world represents both a challenge and an opportunity for South African Life Insurers that, despite current economic difficulties, are becoming increasingly competitive. The challenge is to provide insurance services to consumers who expect to interact via both digital and non-digital channels, and to cross over between them without interruption. The opportunity is to use digital technology to reduce operating costs and increase customer intimacy by analysing the increased information available.

Global leaders that source, consolidate, analyse and make fact-based decisions on this data outperform their peers in this rapidly changing market. Fact-based decisions help insurers to increase sales, reduce risk, improve product pricing and enhance the customer experience.

We, at BSG, believe that South African Life Insurance companies that find the story in the data will be the winners in the long run.

What are Life Insurance Companies doing to address these challenges

Leading international Life Insurance companies are already leveraging big data to make informed, fact-based business decisions to respond timeously to changing market dynamics. There are several key practices that we, at BSG, believe are critical in order to enable our clients to differentiate themselves in the local market:

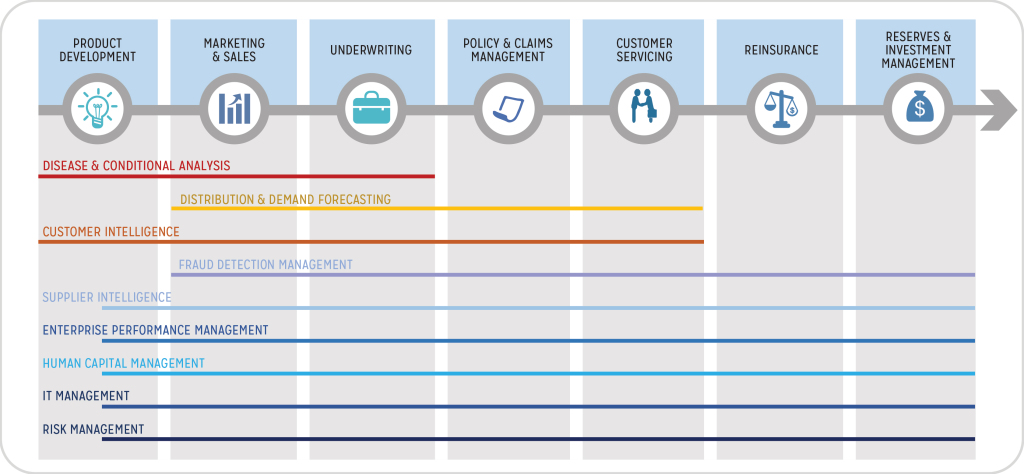

Predictive Analysis

Predictive analytics helps predict future outcomes and can be used to assess, control and improve the risks associated with underwriting and claims, marketing and pricing and the reserving process. It can be used to strengthen customer relationships by helping insurers understand their customers and, subsequently, meet or exceed their expectations.

Risk Analysis

Risk analytics can significantly improve the quality of decision-making processes and can enable more proactive risk-monitoring. Most importantly, risk analytics can assist in improving compliance capabilities and dealing more effectively with an increasingly complex regulatory environment, e.g. capital calculation models, governance, Own Risk and Solvency Assessment.

Distribution and Demand Forecasting

Collection, storage and real-time analysis of the data at every interaction point with customers and distribution partners can help ensure instant detection of opportunities for cross selling and customer satisfaction and retention.

Targeting customers and offering better lead management and one-on-one marketing campaigns enables agents to offer more holistic advice. Additionally, advanced statistical techniques allow for accurate forecasting of sales and demand.

Fraud Detection

Data analytics and predictive modelling can be used to detect fraud and help uncover sophisticated fraud rings. Modelling past fraudulent incidences, behaviours, profiles and segments, matching social network and machine analysis can help insurers understand the indicators and propensities for fraudulent behaviours associated with a claim, claimant or insured party

Customer Intelligence

End-to-end supply chain data collection, storage and Analysis of both internal and external customer data resulting in improved segments and profiles of customers, real-time automation and optimisation of campaigns for acquisition, retention and accurate pricing growing wallet share of existing clients.

Enterprise Performance Management

The ability to consolidate real-time data across customer, operations, risk and human capital from multiple sources into a single view enables better performance management, using KPIs and dashboard visualisation approaches. Dashboarding also takes into account the User Experience (UX) principles for deployment across the enterprise.

Supplier intelligence

Analysing suppliers’ spending habits using a data-driven approach to predict future spend, rationalisation and optimisation of terms, buying patterns and behaviours.

Human Capital Management

Analysing internal and external data to build a single view of the employee with improved insights to factors influencing behaviour and trends and empowering management to attract and retain top talent.

Disease and Condition Analysis

Analysing internal data, past treatment outcomes, family conditions, data from medical databases as well as the latest medical research can be used to predict outcomes for individual policy holders. This data can decrease the cost and intrusiveness of life insurance underwriting and administrative overheads of various medical tests. More accurate life expectancy modelling and possible voluntary sharing of customer data, could allow for more accurate product pricing and improved product profitability.

To download a printable version of this article, click here.