How lean start-up principles are changing the face of business consulting

For years the world of business start-ups followed a strict model: conceptualise an idea, write a business plan, seek out investors, and if you are able to gather sufficient investment capital, develop your product or service and go to market. With this approach entrepreneurs are faced with the daunting prospect of not knowing if sufficient market demand exists to make their business viable until it has been launched, which in 75% of cases is too late. This model bases the success or failure of a business on a number of assumptions made by the entrepreneur, potential investors and marketers. These assumptions often completely miss the mark when the business is finally launched and only on the rare occasion that the assumptions are at least in part correct, the business launches successfully. In most cases however, years have passed since the idea was conceptualised and thousands, if not millions of Rand has been spent, leaving the entrepreneur with enormous loans to pay off or investors to pacify.

For years the world of business start-ups followed a strict model: conceptualise an idea, write a business plan, seek out investors, and if you are able to gather sufficient investment capital, develop your product or service and go to market. With this approach entrepreneurs are faced with the daunting prospect of not knowing if sufficient market demand exists to make their business viable until it has been launched, which in 75% of cases is too late. This model bases the success or failure of a business on a number of assumptions made by the entrepreneur, potential investors and marketers. These assumptions often completely miss the mark when the business is finally launched and only on the rare occasion that the assumptions are at least in part correct, the business launches successfully. In most cases however, years have passed since the idea was conceptualised and thousands, if not millions of Rand has been spent, leaving the entrepreneur with enormous loans to pay off or investors to pacify.

As the global economy began to contract in the early 2000’s and venture capital firms became more prudent about where they invested their money, entrepreneurs began to realise that if they were to be successful, they needed a new approach. And so the concept of the “lean start-up” came into being. A methodology that ‘favours experimentation over elaborate planning, customer feedback over intuition, and iterative design over traditional “big decision up front” development’ (Blank, 2013:66), lean start-up relies on the principles of failing fast and continuous learning to increase the success rate of start-ups. But don’t let the name fool you, lean principles are equally as applicable to established big businesses as they are to start-ups. By following lean principles, big businesses have been able to significantly reduce risk exposure and costs involved in new product or service launches as well as market and geographic expansions.

As the global economy began to contract in the early 2000’s and venture capital firms became more prudent about where they invested their money, entrepreneurs began to realise that if they were to be successful, they needed a new approach. And so the concept of the “lean start-up” came into being. A methodology that ‘favours experimentation over elaborate planning, customer feedback over intuition, and iterative design over traditional “big decision up front” development’ (Blank, 2013:66), lean start-up relies on the principles of failing fast and continuous learning to increase the success rate of start-ups. But don’t let the name fool you, lean principles are equally as applicable to established big businesses as they are to start-ups. By following lean principles, big businesses have been able to significantly reduce risk exposure and costs involved in new product or service launches as well as market and geographic expansions.

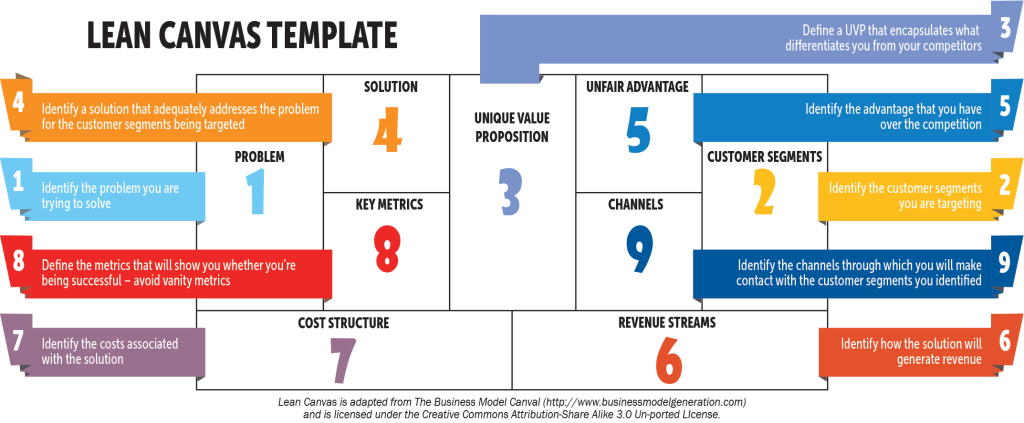

In a traditional start-up, entrepreneurs put together a complicated business plan based on months of research and planning and then approach potential investors with their business plan in order to secure the necessary funding for the business. In the lean start-up approach entrepreneurs start with a series of untested hypotheses, which they summarise in a framework called a business model canvas[1]: a diagram of how the business intends to create value for itself and its customers (Blank, 2013:67).

Where traditionally, entrepreneurs would only test the assumptions about their product when taking it to market, the lean start-up approach tests these assumptions, or hypotheses, up front by getting feedback from potential users, purchasers and partners on all elements of the business model canvass (Blank, 2013:67).

Traditional start-ups tend to take only the final product to market, whereas lean start-ups quickly develop what they call the minimum viable product[2] (MVP). This is used to seek immediate customer and user feedback, which is then used to revise the hypotheses and adjust the product. This repeated process is what is known as agile development, and is borrowed from the software development industry (Blank, 2013:67). Agile development is based on early and continuous development of solutions, ongoing testing and adaptation and continuous learning based on previous iterations of the product.

In the old days, especially at the height of the tech boom, entrepreneurs were so concerned about their ideas being stolen that they worked largely in secret before dropping their ‘fully-formed’ product on the market. Some products were quickly adopted by users and became the technology of choice and others failed miserably, or came too late. Lean start-up values the principles that customer feedback is more valuable to a business than secrecy and that constant feedback yields better, more scalable results (Blank, 2013: 68). As lean principles gain traction in the world of start-ups, so established businesses are beginning to see value in them when launching new products or service offerings, or simply better tailoring their existing offerings. The same is true when looking at business consulting.

Within an established organisation, applying the principles of the lean start-up to executing a business model for an emerging business area/capability is far more cost effective than developing a strategic plan based on well-researched assumptions. This hypothesis has changed the way BSG approaches business operations improvement consulting.

At BSG, by following the build-measure-learn approach, we are able to offer our customers significant confidence and value on a substantially reduced time scale. Similarly, by coupling these principles with those of agile development and user experience design, our consultants are able to ensure early and continuous delivery of collaboratively developed solutions and value adds throughout the project life-cycle. Additionally these solutions are tested and validated with real customers on an ongoing basis.

By utilising the key principles of the lean start-up, such as customer development and problem/solution interviews, we are able to help our clients to invest in better ideas by ensuring that identified opportunities confidently answer certain key questions. Firstly, is this a problem worth solving? Secondly, does the solution adequately address the problem? And finally, will the market buy into the solution, and this includes the effort required for potential customers to change their status quo? By following this approach, BSG consultants are able to more clearly define the requirements and scope of an opportunity as well as to determine if there is sufficient market desire to make the opportunity worth pursuing. If it is determined that the opportunity is potentially viable, consultants collaboratively develop a business canvas model for the opportunity. Through this process, we are able to reduce our client’s risk-exposure by converting assumptions into facts. The MVP can then be developed and tested in iterations ensuring the opportunity is refined, and in some cases, redefined and ultimately executed.

In many cases, start-up businesses are better positioned than big businesses when it comes to determining the success or failure of a venture. Big businesses often end up subsidising bad business ideas with good ones as there is limited visibility of failure or a lack of success. Conversely, start-ups immediately recognise the pitfalls of the idea and in most cases exhaust their funding prospects. By following the principles of the lean start-up approach, BSG is able to guide our clients to make more informed decisions about perceived business opportunities.

With almost two decades of industry experience, BSG is the perfect partner to help businesses investigate, develop and capitalise on new opportunities, and to refine their existing capabilities to better suit market and customer requirements. We have been an integral partner in the delivery of over 500 projects to businesses across a wide variety of industries including, retail and investment banking, insurance, mobile money, telecommunications, and oil and gas. At BSG we have a proven track record of guiding our clients to success by developing authentic relationships based on tested results and trust. BSG has delivered successful interventions across a variety of environments and levels of complexity despite various challenges.

From whiteboard to benefit, BSG asks the right questions and delivers quality end-to-end solutions designed to create positive change for our clients and their customers. Over the next ten years we aim to make a difference in the lives of others by positively impacting 100 million of our clients’ customers, through the value created by our consulting services. At BSG we advise, we don’t prescribe.

References:

Ries, E. (2011) The Lean Startup, London: Portfolio Penguin

Maurya, A. (2012) Running Lean: Iterate from Plan A to a Plan That Works, O’Reilly Media

Blank, S. (2013) Why the Lean Start-Up Changes Everything, Harvard Business Review, May 2013, pp. 65-72.

Cooper, B. and Vlaskovits, P. (2010) The Entrepreneur’s Guide to Customer Development, Cooper-Vlaskovits

[1] The business model canvass lets you look at all nine building blocks of your business on one page (key partners, key activities, key resources, value propositions, customer relationships, channels, customer segments, cost structure and revenue streams) (Blank: 2013: 66).[2] The minimum viable product is a product with minimal functionality that resolves the problem to a degree such that users are willing to pay for it (Cooper & Vlaskovits, 2010:26).

To download a printable version of this article, click here.